This can be a section from the Ahead Steerage publication. To learn full editions, subscribe.

This morning, I had the nice fortune of interviewing Jens Nordvig.

The interview shall be out tomorrow, however I needed to offer a teaser round one thing extremely necessary: Fed independence.

Nordvig is the founding father of Exante Information and was beforehand managing director at Goldman Sachs, senior funding affiliate at Bridgewater, and head of mounted revenue analysis at Nomura.

At this level, everybody is aware of that President Trump doesn’t like Jerome Powell very a lot and thinks rates of interest needs to be meaningfully decrease.

Particularly, the lens of criticism has shifted from the standard twin mandate of the Fed — secure costs and most employment — towards what fiscal authorities view as a extra related mandate, managing the debt load of the US authorities. One of many key arguments being made is that the Fed ought to decrease rates of interest in order that curiosity funds on US debt come decrease, thereby reducing the fiscal deficit.

This subordination of financial coverage to fiscal priorities of debt load administration is what I view because the extra appropriate definition of fiscal dominance.

Fiscal authorities set coverage, and financial authorities are there merely to make it the least painful. Nothing extra, nothing much less.

The final time that this occurred was within the Forties, when the Fed formally employed yield-curve management to cap charges at sure ranges and its major goal was to purchase US debt and handle the debt load. This regime led to earnest with the Fed Treasury accord of 1951, which reinstilled Fed independence. Ever since these accords, we’ve been in an period of financial dominance.

We at the moment are within the early innings of this transition.

The first threat related to dwindling Fed independence is the potential for inflation expectations to develop into unanchored. In easy phrases, this appears like inflation considerations being instilled in society and a typical realization that the Fed can’t get a significant deal with on these inflation expectations.

In observe, the standard objective of central banks having a 2% goal for inflation serves as a codified intention to forestall inflation expectations turning into unanchored.

Sadly, this gradual however regular erosion of Fed independence by the Trump administration is already starting to percolate into inflation expectations, and the chance of those turning into unanchored is rising meaningfully.

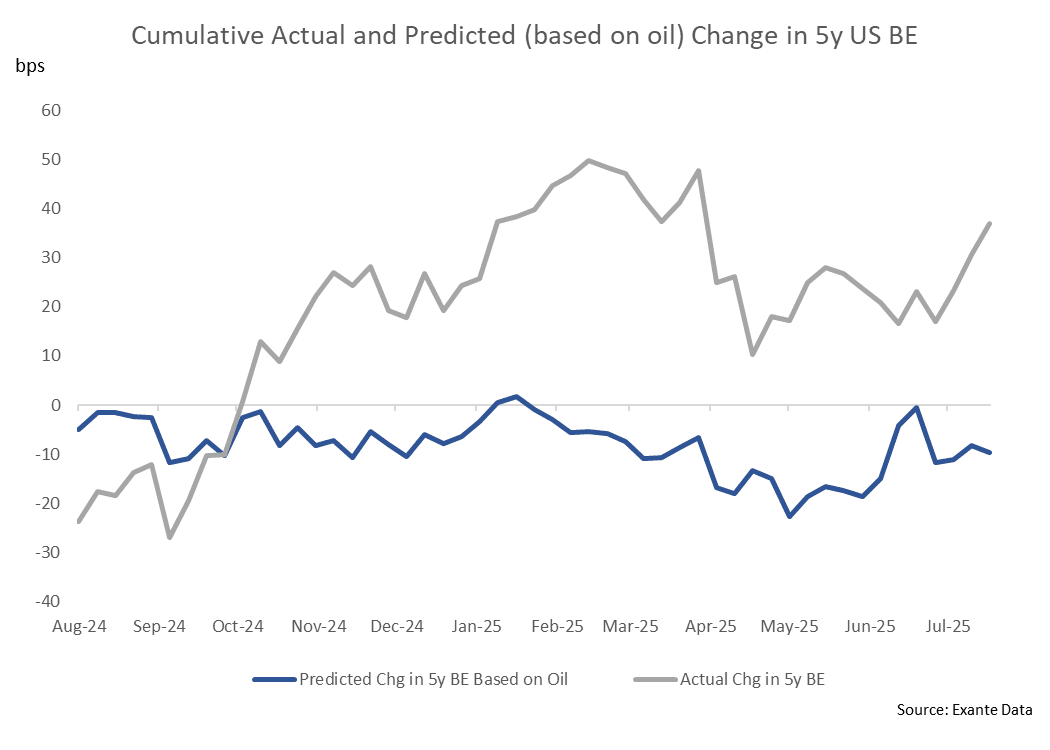

Jens introduced an interesting chart to our dialogue that highlights this rising dynamic.

The chart under exhibits the cumulative and predicted adjustments in five-year US breakeven charges, each as predicted by adjustments in oil and unbiased variables: