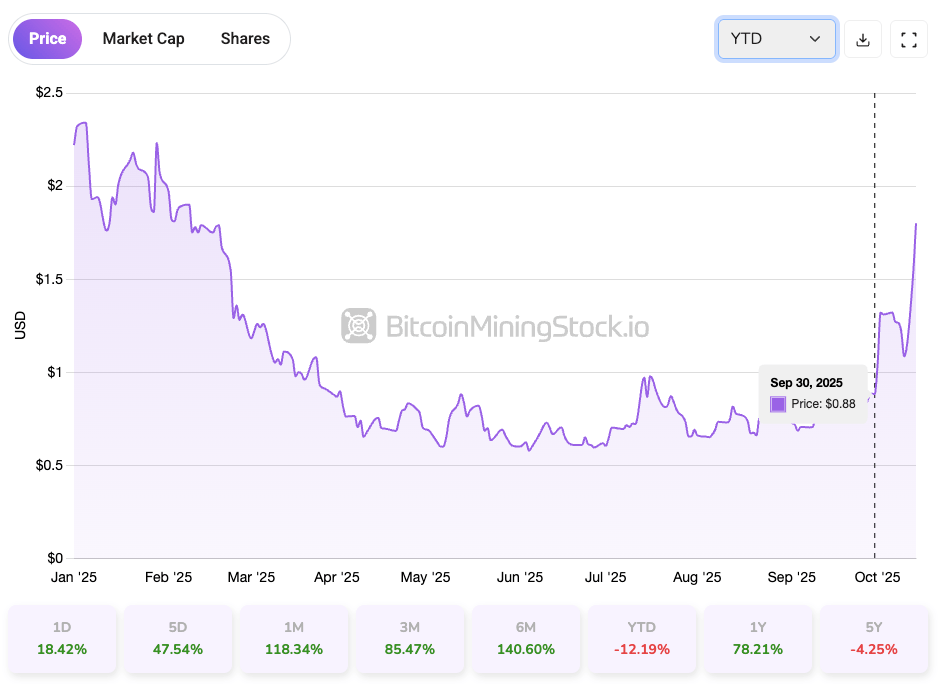

CAN is again above the $1 mark after buying and selling under it for months. With a landmark 50,000-unit ASIC order and new partnerships with SLNH and Luxor, sentiment is shifting quick. So is that this a sensible entry level now?

The next visitor submit comes from BitcoinMiningStock.io, a public markets intelligence platform delivering knowledge on corporations uncovered to Bitcoin mining and crypto treasury methods. Initially printed on Oct. 15, 2025, by Cindy Feng.

A number of weeks in the past, a few of my followers pinged me about Canaan Inc. (NASDAQ: CAN). They argued its share value was a cut price in comparison with its OG friends – lots of whom have posted triple-digit beneficial properties this yr. Whereas these names have dominated headlines, Canaan has been quietly staging a comeback since final week.

Identified primarily for its Avalon ASIC mining machines, Canaan spent most of 2025 out of sync with the market’s fixation on HPC and AI infrastructure. On prime of that, the continuing U.S.-China tariff battle pushed its inventory under $1 for months, elevating actual considerations a couple of potential Nasdaq delisting.

However one thing shifted just lately. Since September 30, the inventory has clawed its manner again above $1 and stored climbing, due to a wave of company developments. Regardless of nonetheless displaying a -12.19% YTD efficiency, the momentum is clearly turning. So the actual query is whether or not that is the sensible time to leap in. Let’s break it down.

Firm Overview: Extra Than Simply an ASIC Maker

Based in 2013, Canaan Inc. is a expertise firm headquartered in Singapore, with deep roots in China’s semiconductor ecosystem. Finest recognized for designing and manufacturing Avalon-branded ASIC Bitcoin mining machines, Canaan has step by step remodeled from a pure-play {hardware} supplier right into a extra diversified participant within the crypto mining sector.

Self-Mining

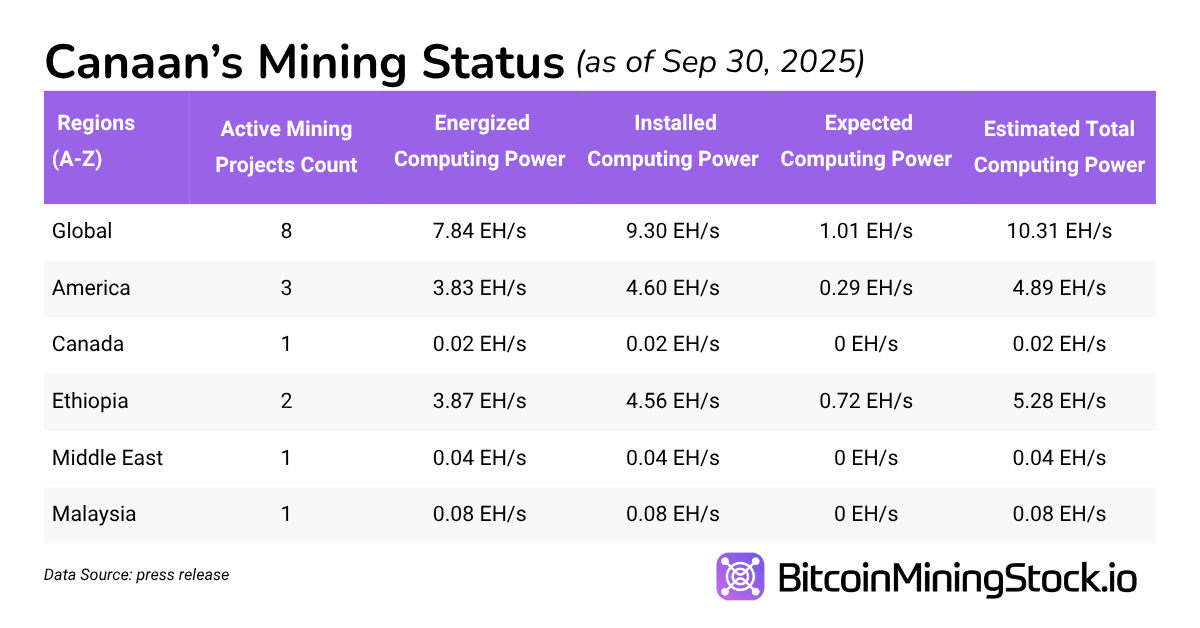

As of September 2025, Canaan operates 9.30 EH/s of hash price, primarily within the U.S. and Ethiopia. The self-mining capability can scale to 10.31 EH/s as soon as pending ASICs deliveries are put in. Since January this yr, Canaan reported ~87 bitcoin mined monthly. The income from this enterprise section has been growing constantly since Q2 2024.

Bitcoin Treasury

Canaan holds 1,582 BTC as of September 30, 2025. Based on its Q2 incomes presentation, BTC is collected by way of a combine of self-mining, {hardware} gross sales funds, and spot market purchases. The corporate additionally actively makes use of its Bitcoin holdings as collateral to fund R&D and {hardware} manufacturing, and even allocates a portion to short-term interest-bearing accounts to generate yield. Its Bitcoin treasury continues to be within the early phases, per CFO James Jin Cheng. Anyway, its Bitcoin treasury already ranks because the thirty fifth largest amongst public corporations globally on our web site. When it comes to publicity, Canaan’s Bitcoin holdings characterize 20.29% of its market cap, a ratio that’s much like some bigger gamers like Riot Platforms and CleanSpark.

Retail Dwelling Mining Tools

Canaan has just lately launched pre-assembled Avalon Miner kits focused at house miners and small-scale operations. These kits are designed for simple deployment and embody plug-and-play containerized items. Whereas present income from this line stays marginal, it might strengthen model visibility and assist scale back reliance on unstable institutional demand cycles.

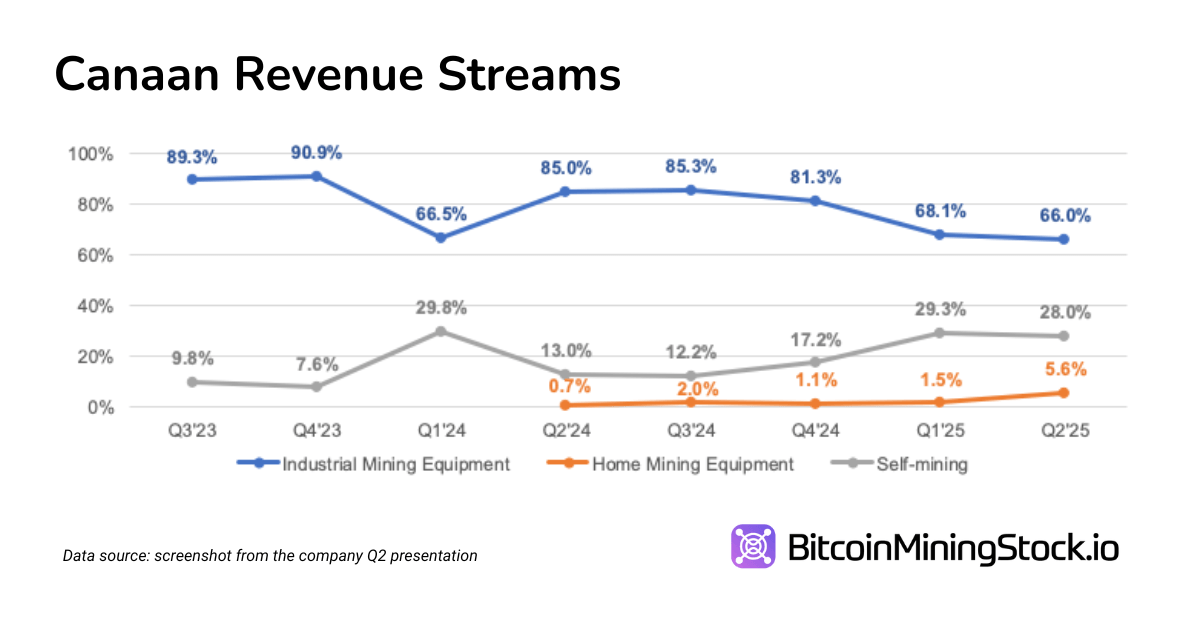

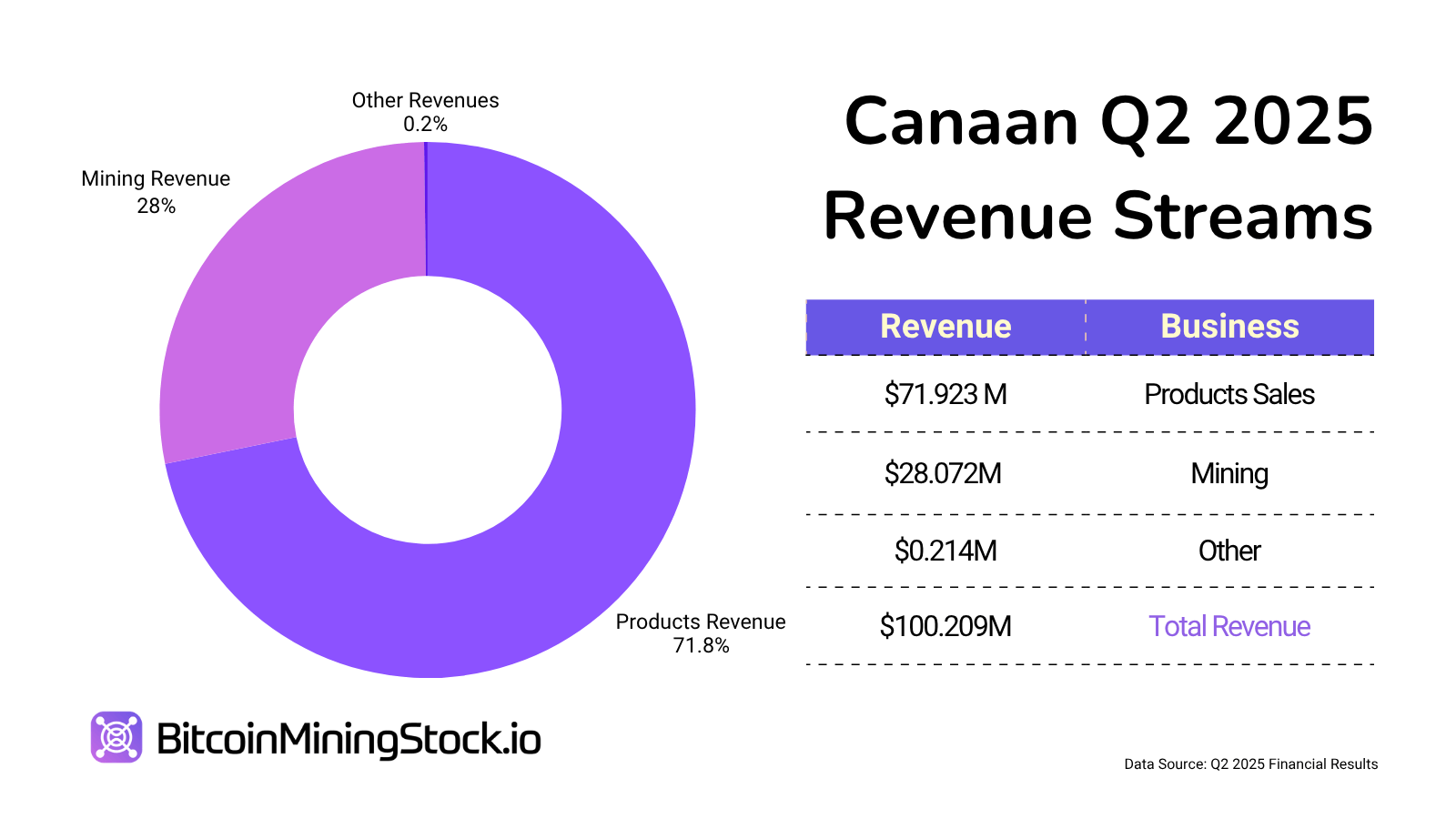

In Q2 2025, Canaan generated $73.9M in whole income. Of that, 71.7% got here from {hardware} gross sales, 28.1% from mining operations, and fewer than 1% from different providers.

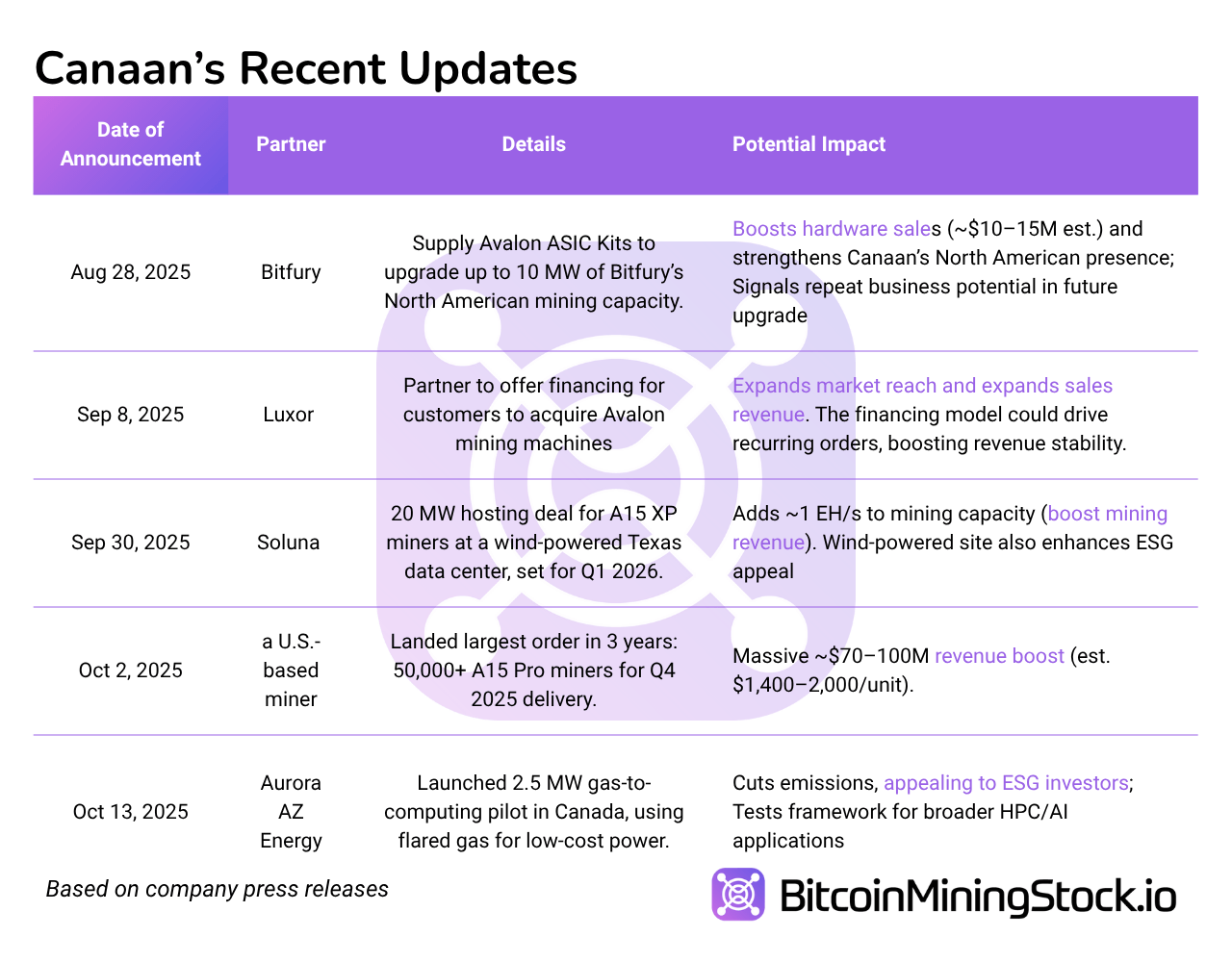

Current Catalysts: The Momentum Is Constructing

Investor sentiment round Canaan is shifting, due to a string of enterprise wins and strategic partnerships. The current updates paint an image of an organization gaining traction, every deal not solely provides to top-line potential but additionally helps gas renewed investor curiosity. To make issues simpler to trace, right here’s a timeline of key enterprise updates:

Seen collectively, these developments recommend that Canaan is doubling down on North America. A number of offers level to a renewable power pivot, which might enchantment to ESG-focused traders. Most significantly, these strikes will present up within the numbers. The corporate is guiding for $125–145M in Q3 income, presenting 25%-45% QoQ development.

Is CAN Inventory a Cut price at $1.80?

At $1.80, Canaan’s valuation appears to be like compelling in comparison with friends, however let’s see whether or not it’s nonetheless a cut price.

As of Oct 15, 2025, Canaan holds a market cap of $881.96 million. After adjusting for $179 million in Bitcoin (1582 BTC x $112,833) and 11.63 million in Ethereum (2830 ETH x $4111) , $65.9 million in money, and $268.5 million in debt, the enterprise worth (EV)* sits at round $894 million. This gives a cleaner view of the corporate’s core working worth, excluding treasury property.

*For my calculation: EV = Present Market Cap + Complete Debt – Money & Money Equivalents – Truthful Worth of Bitcoin Holdings – Truthful Worth of Ethereum Holdings. Debt and money figures are sourced from the newest quarterly report, whereas the honest worth of crypto property relies on present spot costs and the corporate’s most up-to-date disclosed holdings.

Canaan has a guided Q3 2025 income between $125–145 million, implying an annualized income run price of $500–580 million. Based mostly on these projections, the corporate trades at an EV/income a number of of 1.5x–1.8x, under the two.5x–4x vary usually seen amongst U.S.-listed friends throughout bullish cycles.

From a profitability lens, Canaan posted $25.3 million in adjusted EBITDA in Q2, annualizing to roughly $100 million. This interprets to an EV/EBITDA a number of of ~8.9x, modest in comparison with top-tier miners buying and selling at 10–20x underneath favorable market situations. That leaves room for a number of enlargement, if margins maintain or investor sentiment strengthens.

On an asset foundation, the corporate reported ~$484.5 million in web property excluding crypto and $592.1 million together with its crypto holdings. This ends in a price-to-book (P/B) ratio of two.7x to 4x relying on remedy of digital property. These aren’t deep-value ranges, however they’re additionally not overstretched, particularly provided that a lot of Canaan’s current partnership offers haven’t totally hit the financials.

In the end, at $1.80, the inventory will not be deeply discounted but additionally not aggressively priced. The market is recognizing improved fundamentals and near-term income visibility, however has not but assigned a premium for development or broader strategic upside.

Last Ideas

Canaan is evolving from a {hardware} provider to a extra vertically built-in crypto mining participant, with rising self-mining operations, a significant crypto treasury (1,582 BTC and a pair of,830 ETH), and increasing world partnerships. The current 50,000-unit miner order ought to increase income meaningfully within the coming quarters and assist enhance valuation metrics..

That mentioned, challenges stay. Canaan posted an $11.1 million web loss in Q2, and until Bitcoin costs keep elevated or price efficiencies kick in, bottom-line profitability could stay underneath strain. Excessive working prices and depreciation proceed to weigh on margins.

Geopolitical dangers additionally linger, significantly round U.S. tariffs on Chinese language tech exports. Whereas Canaan is working to mitigate this by way of new manufacturing strains within the U.S. and Malaysia, execution threat stays.

In the end, the subsequent few quarters-particularly Q3 outcomes (guiding $125–145M), Bitcoin value course, and community issue developments, will possible decide whether or not Canaan earns a market rerating. For traders betting on a broader crypto bull cycle, this inventory affords potential-but not with out its dangers.