CleanSpark delivered an impressive monetary quarter, however its market efficiency didn’t mirror the identical energy. This evaluation breaks down key financials, operational insights, and strategic instructions to grasp the complete image.

CleanSpark Govt Overview: Sturdy Execution Amid Market Ambivalence

The next visitor publish comes from Bitcoinminingstock.io, the one-stop hub for all issues bitcoin mining shares, instructional instruments, and business insights. Initially printed on Feb. 20, 2025, it was penned by Bitcoinminingstock.io creator Cindy Feng.

Whereas doing analysis for my Bitcoin Mining Annual Report again to Dec 2024, CleanSpark stood out with a number of key metrics, comparable to gross margin, hash price enlargement, M&A actions, and fleet upgrades. At the moment, I believed the corporate was positioned for a powerful 12 months forward—assuming Bitcoin’s worth continued its upward momentum.

Screenshot from the annual report (co-authored with Nico Smid from Digital Mining Options)

Nonetheless, following CleanSpark’s fiscal Q1 2025 earnings name on February 6, 2025, the corporate’s inventory worth remained flat and even declined. This market response raised some questions for me: What numbers shocked traders? Did the corporate present steerage that involved traders? Let’s take a better take a look at the numbers and break down what may be occurring.

Monetary Highlights: Income & Profitability Surged

CleanSpark’s fiscal Q1 2025 (Oct 1 – Dec 31, 2024) was an impressive quarter financially, demonstrating sturdy income development and powerful profitability, pushed by Bitcoin’s worth improve and improved operational effectivity.

Key Revenue Assertion Metrics:

- Income: $162.3 million (+120% YoY) vs. $73.8 million in Q1 2024. This was primarily pushed by a rise in Bitcoin worth, offset by a decrease variety of Bitcoin mined because of the halving occasion in April 2024

- Internet Revenue: $246.8 million (+854% YoY) vs. $25.9 million in Q1 2024, largely dues to truthful worth Bitcoin revaluation.

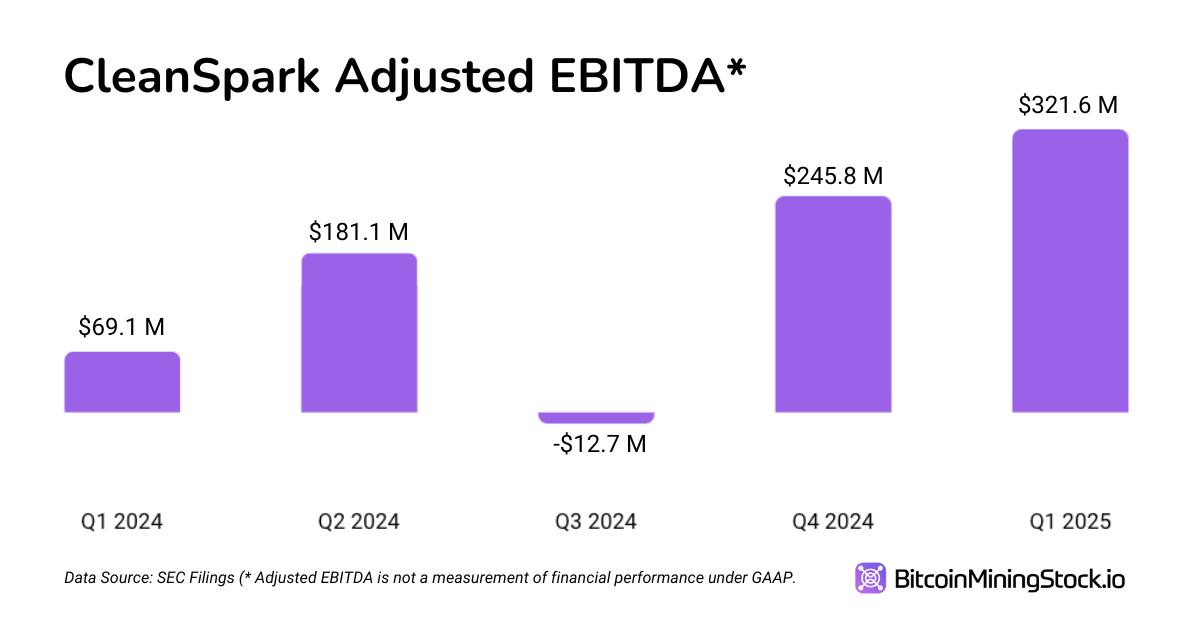

- Adjusted EBITDA: $321.6 million from $69.1 million, setting a brand new report. (*This reported quantity embody $218.2 million truthful worth acquire)

- Gross Margin: 57%, barely decrease than 60% YoY resulting from elevated operational prices (significantly power prices and mining infrastructure enlargement)

- Bitcoin Manufacturing: 1,945 BTC, down barely from 2,020 BTC in Q1 2024 because of the Bitcoin halving occasion in April 2024.

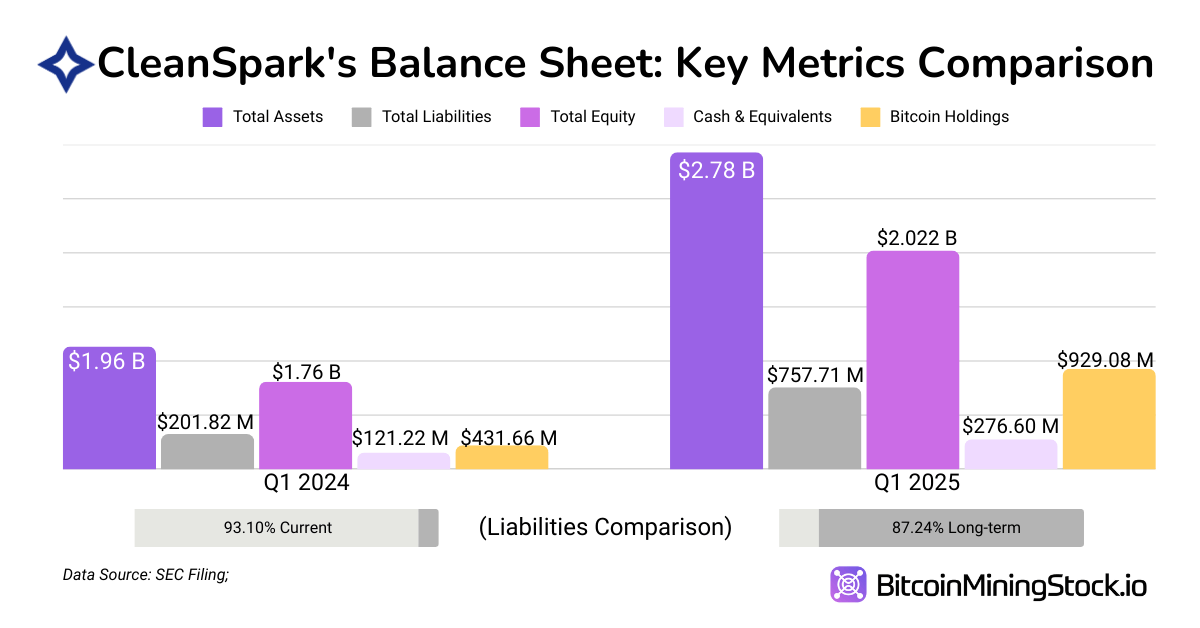

Key Stability Sheet Metrics

- Complete Property: $2.78 billion (+41.6% YoY), vs $1.96 billion in Q1 2024. Largely pushed by improve in Bitcoin holdings and information middle expansions & new mining infrastructure.

- Complete Present Liabilities: $96.7 million dropped from $187.9 million, primarily resulting from mortgage repayments ($52.2M paid off)

- Lengthy-term Liabilities: $641.4 million (vs $7.2M), primarily resulting from new convertible debt issuance

- Stockholders’ Fairness: $2.02 billion (+14.8% YoY), vs $1.76 billion in Q1 2024

- D/E ratio: 0.32 (vs 0.08), indicating that CleanSpark has considerably elevated its leverage over the previous 12 months, by taking over extra debt to fund development.

Key Money Circulation Metrics

- Working Money Circulation: $119.5 million internet money utilized in operations

- Investing Money Circulation: $255.9 million used (together with $126.9 million for brand spanking new miners and $57.4 million for fastened belongings)

- Financing Money Circulation: $531.1 million inflows (together with $186.8 million in fairness choices +$635.7 million in mortgage proceeds-$145 million treasury inventory repurchases)

- Firm expects money, BTC holdings, and operational money circulate to be adequate for 12+ months, however financing could also be wanted for additional enlargement

Valuation Metrics & Enterprise Worth

CleanSpark’s market cap at the moment stands at $2.61 billion (Advertising closing on Dec 31, 2024). To raised perceive its valuation, I compiled a couple of key monetary metrics:

- Enterprise Worth (EV): $2.16 billion (Market Cap + Debt – Money & Bitcoin Holdings).

- EV/EBITDA Ratio: 6.71x ($2.16B / $321.6M), which is comparatively low for a high-growth Bitcoin miner.

- P/E Ratio: 10.57x ($2.61B / $246.8M), suggesting the corporate is buying and selling at a reduction in comparison with tech development shares.

- BTC Holding as % of Market Cap: 35.6%, that means greater than one-third of its valuation is backed by Bitcoin holdings alone.

I’ll come again and evaluate with different miners, who’ve an identical operational scale, as soon as information turns into out there.

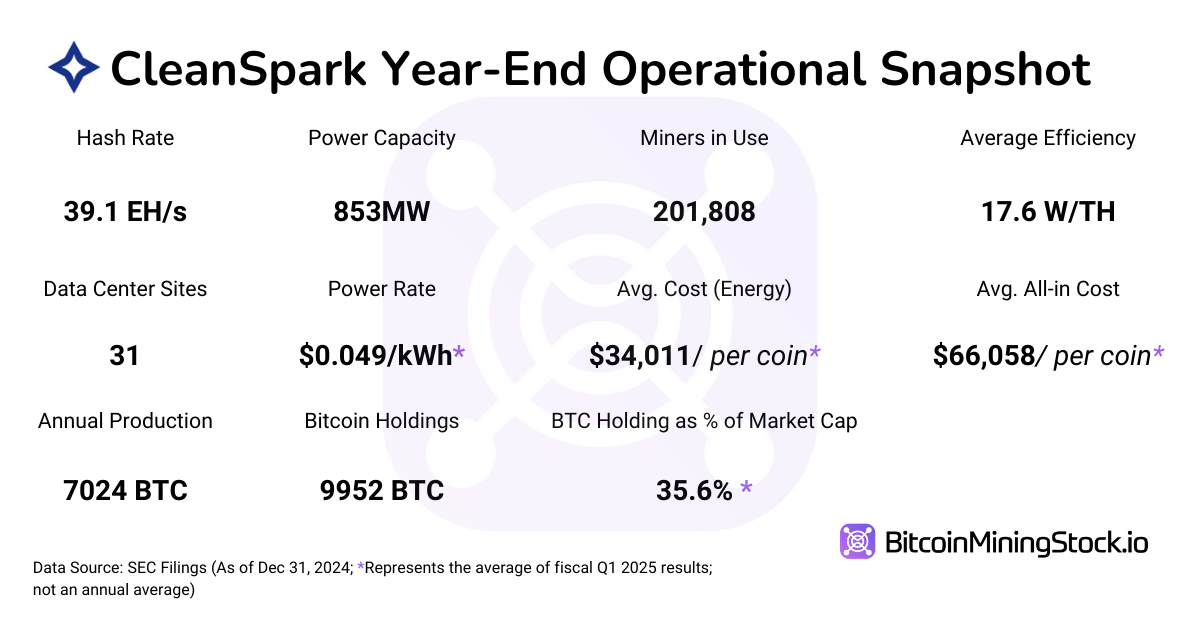

Operational Metrics: Hash Price Development & Effectivity Enchancment

Key Hash Price & Effectivity Metrics:

- Hash Price: 39.1 EH/s (4.87% of world hashrate), a 4x improve YoY (10.0 EH/s in Q1 2024).

- Working miners: 201,808 in operation, up from 88,559 YoY.

- Common Effectivity: 17.6 W/TH, improved from 26.4 W/TH YoY.

- Bitcoin Manufacturing Value (Direct Power Value Per BTC at owned Facility):$34,011, up from $12,808 YoY.

- Complete Value Per BTC (Together with Depreciation & Financing): $66,058, up from $24,429 YoY.

Power Value Evaluation & Mitigation Methods

- Energy price: $0.049/KWh (vs. $0.044/KWh YoY).

- 40.4% of Bitcoin income is used for power prices, up from 35% YoY.

- Hurricane Helene led to momentary operational curtailments, decreasing effectivity.

- Power Mitigation Methods:

- Diversified Geographic Enlargement: New websites in Wyoming, Tennessee, and Georgia with decrease energy charges.

- Excessive-Effectivity Mining Rigs: Deployment of S21 XT immersion models for decrease energy draw.

- Versatile Energy Contracts: Agreements to optimize power utilization and price however stays uncovered to cost volatility

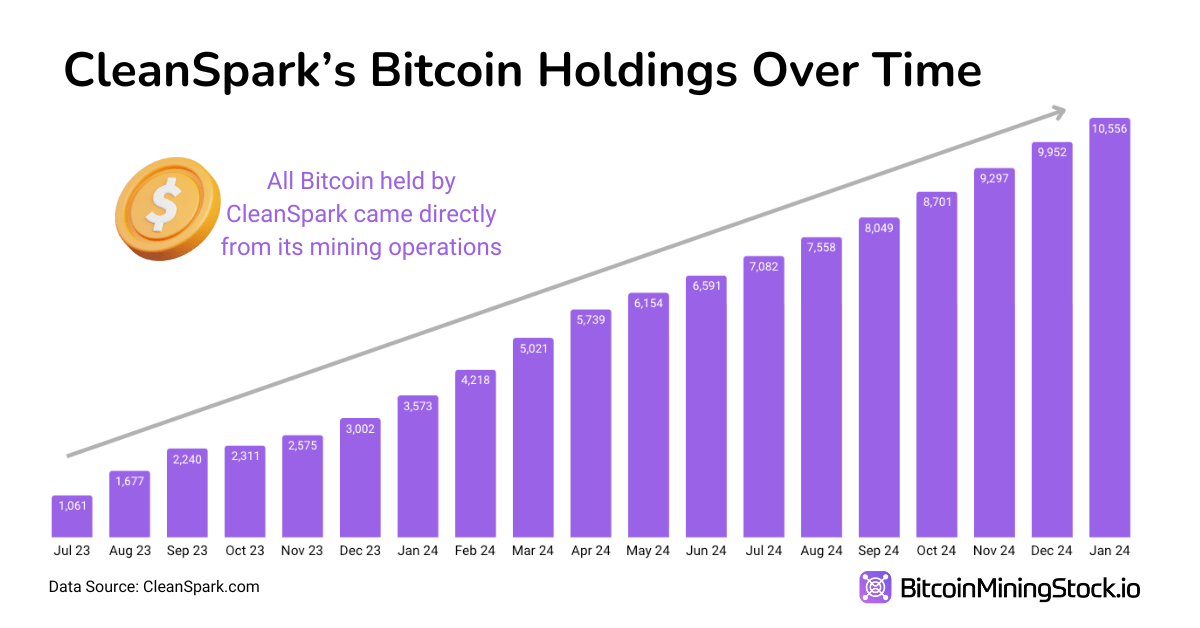

Bitcoin Holding & Treasury Technique: HODL Over Promote

BTC Treasury:

- Complete Bitcoin Held: 9,952 BTC (valued at $929 million; up from 6,819 BTC in contrast with the earlier quarter).

- 99% of BTC in chilly storage, 1% in sizzling wallets.

- BTC Bought Throughout the Quarter: 3,413 BTC ($3.4 million price) in comparison with 43,300 BTC ($43.3 million) in Q1 2024

- BTC Used as Collateral (to the Coinbase): $8.86 million transferred, $129.18 million retrieved from collateral accounts.

- Funding Operations: Relied on exterior financing ($635.7M convertible debt) as a substitute of BTC gross sales.

- No BTC Lending or Yield Methods Reported.

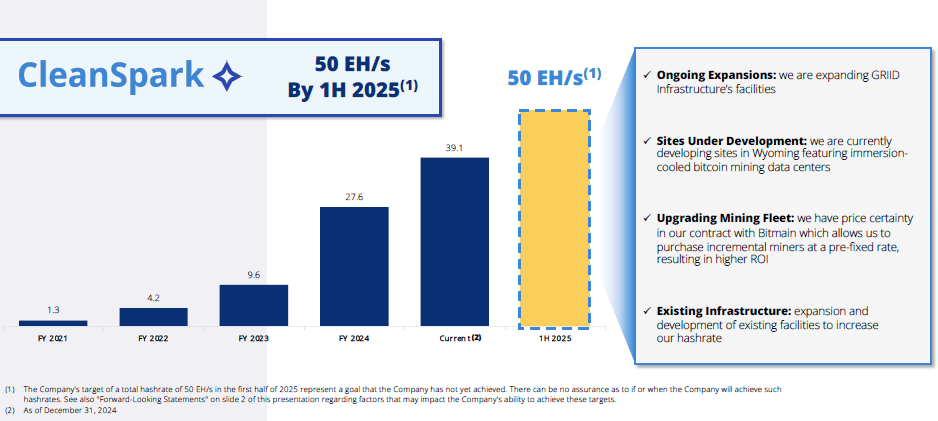

Enlargement & M&A: Scaling Up for 50 EH/s

Development & Enlargement Plans:

- Purpose: 50 EH/s by mid-2025, with potential enlargement to 60 EH/s.

-

New Mining Websites Acquired:

- Tennessee Web site: $29.9M funding.

- Mississippi Web site: $3M funding, plus $2.9M for infrastructure.

-

Fleet Development:

- 60,000 S21 miners secured, with an choice to purchase 100,000 extra at $21.50/TH, 37% under market worth.

- 285,098 complete miners owned, with ~83,290 pending deployment.

CleanSpark’s Hash Price Development Roadmap (screenshot from the corporate presentation)

Ideas: The Large Image & Key Issues

By taking a look at numbers from the monetary report, I nonetheless imagine CleanSpark holds a powerful place within the Bitcoin mining sector. The corporate positions itself as a premier American Bitcoin miner, which might grow to be much more advantageous underneath the present U.S. administration.

Nonetheless, my major concern stays Bitcoin’s worth motion. Traditionally, CleanSpark’s inventory worth is tightly correlated with BTC efficiency. If Bitcoin surges, CleanSpark can grow to be extra enticing; but when BTC stagnates or dips, CLSK might face large sell-offs.

One other key issue to contemplate is how CleanSpark manages income throughout completely different market cycles. Not like friends diversifying into AI/HPC, CleanSpark stays dedicated to Bitcoin mining. Its CEO stays skeptical of HPC, statingthat “ repurposing a Bitcoin mining facility for high-performance computing is much extra complicated than it could seem”, and reinforcing CleanSpark’s long-term give attention to Bitcoin as an environment friendly, confirmed, and scalable enterprise mannequin. This means the corporate is unlikely to pivot like its friends any time quickly.

That mentioned, the corporate might discover methods to leverage its BTC holdings strategically—maybe via treasury methods that decrease counterparty dangers whereas enhancing monetary flexibility.

In the end, CleanSpark boasts one of many largest mining operations, high vary effectivity, disciplined capital administration and wonderful executions (exceeded their annual hash price goal), and impressive enlargement plans. I at the moment see no robust purpose to be bearish on CleanSpark so long as Bitcoin mining stays a viable business.

Even when we discuss in regards to the present trending Bitcoin Treasury Technique, Cleanspark could be a compelling funding alternative. Compared with Technique (MSTR)- probably the most well-known advocate of this technique, CleanSpark holds a important benefit: they will get hold of Bitcoin at a considerably lower cost (all-in price: $66,058 per coin) by mining. As folks say “When you can mine at a lower cost, why purchase?”